DIGITAL TAX INVESTIGATIONS - HOW AUTHORITIES USE DATA TO CATCH NON-COMPLIANCE

Name: Ishika Thakkar

Registration No.: WRO0783155

City: Vadodara, Gujarat

DIGITAL TAX INVESTIGATIONS - HOW AUTHORITIES USE DATA TO CATCH NON-COMPLIANCE

Abstract

Once upon a time, tax officers needed files, audits, and visits to catch fraud. Now, algorithms do the detective work before the coffee gets cold.

The integration of technology with taxation has transformed India’s compliance landscape from a document-driven regime to a data-driven one. The Goods and Services Tax (GST) system has emerged as one of the most advanced tax infrastructures in the world, leveraging automation, analytics, and artificial intelligence to identify inconsistencies and detect non-compliance in real time.

Through this paper, we explore how the GSTN, ICEGATE, and allied digital systems collaborate to create a transparent, interconnected, and self-regulating tax environment. Drawing from personal experience in the GST department, this study presents practical examples that showcase how the portal itself has evolved into a digital detective — identifying errors, mismatches, and potential frauds before human intervention even begins.

In today’s India, it’s not Big Boss watching you —it’s Big Data.

Introduction – The Rise of the Digital Detective

The traditional image of tax investigation involved files, manual reconciliations, and physical inspections. Today, however, the investigator is digital — a combination of interconnected databases, algorithms, and AI-driven analytics capable of detecting anomalies within seconds.

India’s GST network, backed by the Goods and Services Tax Network (GSTN), integrates data from millions of taxpayers and cross-verifies it across platforms such as ICEGATE, E-Way Bill, and Income Tax systems. The goal is not just to catch defaulters but to make evasion technically impossible.

Interconnected Portals – The Digital Ecosystem

The GSTN has created a seamless interface between various government platforms, ensuring that one database automatically validates the other.

GSTN + E-Invoice Portal

When e-invoices are uploaded, the system checks for duplicates across all return periods.

For instance, while uploading an e-invoice for the October return, an error appeared stating that the same invoice number already existed in the November period — a clear sign of real-time cross-verification by the backend system.

This level of synchronization proves how the database isn’t passive storage — it’s an active analytical engine.

GSTN + ICEGATE + E-Way Bill

These three systems together form the triangular surveillance mechanism of GST.

Any change in the GST portal, such as updating an authorized signatory, automatically updates on ICEGATE.

Shipping bills for export are validated against ICEGATE data.

E-way bill data is continuously compared with GSTR-1 and GSTR-3B figures.

This creates a loop of interdependence where a mismatch in one system instantly alerts another — making the digital web nearly impossible to outsmart.

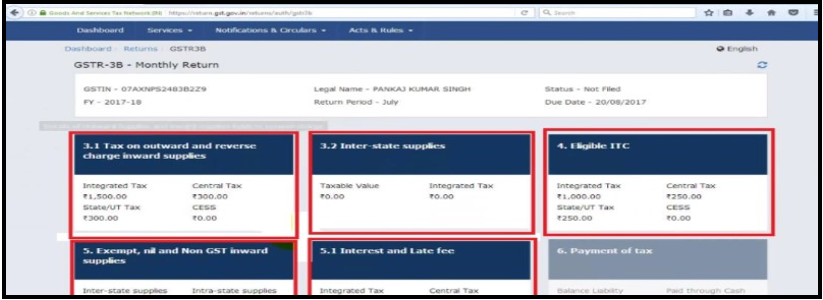

Autofill and Auto-Validation – The Era of Controlled Compliance

The autofill feature in GSTR-3B, derived from GSTR-1 data, ensures that outward supply details can’t be manually altered.

While filing returns, the outward supply values appeared auto-filled and uneditable, revealing how the portal now controls what data is accepted, not the taxpayer.

The system’s logic is simple: you can’t modify what you already declared elsewhere.

This ensures a seamless audit trail and leaves no room for manipulation.

ICEGATE Integration – Customs and GST Talk in Real Time

Imports and exports form one of the most complex data zones in indirect taxation. The synchronization of ICEGATE (Customs portal) with the GST portal ensures:

- Matching of shipping bills and export invoices

- Validation of IGST refund claims

- Automatic import GST data population

For example, while filing export returns, mentioning the shipping bill number allows the system to verify details directly from ICEGATE — a strong safeguard against bogus export claims.

This interlinking has turned the ICEGATE portal into a silent investigation tool. Suspicious discrepancies in declared export value or refund claims trigger automated scrutiny.

AI-Powered Mismatch Detection – DRC-01C Notices

Artificial intelligence embedded within the GSTN system continuously compares ITC claimed in GSTR-3B with ITC available in GSTR-2B.

When a mismatch exceeds the threshold, a DRC-01C notice is issued automatically — without manual officer intervention.

In one instance, a taxpayer received this notice for claiming excess ITC, entirely generated by the system’s algorithm.

This evolution represents a major shift — from reactive enforcement to proactive digital policing.

The E-Way Bill Link – Tracking Goods in Motion

The e-way bill portal is another crucial data source that complements GST returns. By comparing e-way bill values with sales declared in GSTR-1, the system can flag potential suppression of turnover.

For example, a taxpayer might generate e-way bills worth ₹5 crore but report outward supplies of only ₹4 crore. The system automatically flags this ₹1 crore gap as a high-risk mismatch.

The ability to geo-track goods, reconcile invoices, and link movement with tax payment turns the e-way bill portal into a nationwide “GPS of compliance.”

Data Analytics in Action – How the Portal Thinks

Authorities now use pattern recognition algorithms to detect unusual taxpayer behavior. These include:

Spike Analysis: Detecting sudden increases or drops in turnover.

Network Mapping: Tracing connections between fake invoice networks.

Behavioral Profiling: Identifying habitual late filers or those constantly revising returns.

Cluster Comparison: Comparing similar businesses in the same industry to flag outliers.

The system “learns” from past cases — if one fake firm pattern is detected, the algorithm scans for others following similar patterns.

This means tax fraud no longer hides behind paperwork — it hides in data, and the portal knows where to look.

Expansion Beyond GST – The Future of Digital Investigations

The GSTN model has inspired similar data integration across other departments:

Income Tax Portal: Uses AIS/TIS for pre-filled returns.

CBIC & DRI: Use AI for risk assessment of import consignments.

Bank Integration: Helps verify cash-flow consistency with declared turnovers.

PAN-based 360° Analytics: Links all financial activity of a person or entity across departments.

Future developments may include: AI-based predictive compliance scoring, Machine-learning fraud detection, and Real-time cross-verification with payment gateways and UPI transactions. Essentially, the portal is learning to think like an investigator — detecting before questioning.

The Role of Chartered Accountants in the Digital Era

With such high automation, the role of a Chartered Accountant becomes more strategic than clerical.

CAs must now: Interpret system-generated red flags, assist clients in digital reconciliations, use data analytics tools for self-review before filing, and ensure every declaration aligns with the system’s cross-verification logic. We are no longer just return filers — we are data translators between businesses and technology.

Conclusion – From Compliance to Intelligence

The GST portal is not merely a filing interface; it has evolved into a digital detective, constantly watching, comparing, and learning.

Each invoice uploaded, each return filed, and each mismatch corrected adds intelligence to the system — enabling it to detect non-compliance faster and more accurately than ever before.

As future Chartered Accountants, understanding these systems gives us an edge. We become not only compliant professionals but guardians of digital transparency. Because in this new world, data doesn’t lie — it investigates.