IPO UNDER-PRICING IN INDIA:CAUSES, TRENDS AND CASE ANALYSIS

Name: Jeet Kavlekar

Registration No.: WRO0826441

City: Goa

Introduction

Ever wondered why most of the IPOs skyrocket on Day 1? Well the real drama of an IPO often begins after the bell rings and the market opens. That instant jump in share price after an IPO isn’t just a luck it’s underpricing at play. Welcome to the puzzle of IPO underpricing. An IPO Under- pricing is the practice of listing an IPO or an Initial Public Offer at a price below its real value in the stock market.

Causes

1. Attracting Institutional Investor and Long Term Stakeholders

Underpricing helps attract sophisticated Institutional Investor and Long Term Stakeholders who will hold the stock after the initial trading day, providing a stable base for the company’s stock and future funding.

2. Information Asymmetry

Investors do not have the same information as the company and underwriters, therefore in order to attract uninformed or retail investors, IPOs are often priced lower, especially incases young companies, SMEs, or first-time issuers with limited track record. If we take a look at India Context:

- Many Indian IPOs are from family owned or promoter-driven companies where governance standards vary.

- Investors often fear hidden liabilities, aggressive accounting, or promoter opportunism.

- Underpricing acts as an incentive for investors to trust the issue.

3. Securing Investor Participation

A lower initial share price can incentivize a wider range of investors, particularly retail investors to participate in the IPO. This reduces the risk of “Undersubscribed” IPO.

4. Issue size

Smaller IPOs tend to be riskier due to low visibility, limited analyst coverage, and weaker institutional participation. Issuers deliberately set prices attractively to ensure full subscription. Whereas, Larger IPOs are backed by greater institutional interest, stronger media coverage, and deeper regulatory scrutiny. Presence of anchor investors and large QIB allocations leads to more efficient price discovery, reducing the need for underpricing. If we take a look at LIC IPO (2022) it was India’s biggest. Despite hype, it listed flat due to efficient pricing and valuation scrutiny, on the other hand Small-cap IPOs often list at 50–100% premium.

TRENDS

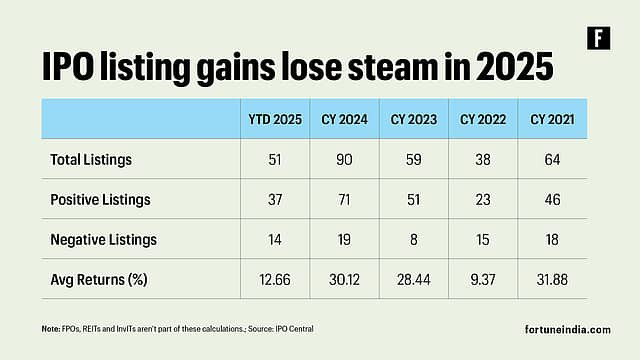

1. Declining Average First-Day Listing Gains

As per the Fortune report (17th Sept, 2025) the average first-day listing return has dropped sharply to about 12.7% in 2025, from ~30.1% in 2024.The listing gains dropped 58% from previous year.

2. SME IPOs Underperform Compared to the Boom of Previous Years

Let’s take a look the Fortune report dated 27th July, 2025, after a robust performance in 2024, small and medium enterprise (SME) IPOs have witnessed a fall in the listing gains in 2025. The average listing gains of 105 SME IPOs across BSE and NSE platforms have dropped to nearly 10%, a steep fall from the around 60% gains recorded last year. Increased market volatility, growing investor caution, and external pressures such as tariff-related uncertainties and geopolitical challenges are to be given the credit.

3. Fundraising Volume Still Strong Despite Cooling Gains

Even though listing gains are lower, the amount raised by IPOs remains high. For FY25, about

₹1,62,387 crore was raised via main board IPOs which is more than 2.5 times the ₹61,922 crore mobilised by 76 IPOs in 2023-24. Of these, over 60% were trading above their issue prices, according to PRIME Database.

4. Market sentiment, global factors impacting underpricing

IPO listing gains in 2025 have halved to 14.6% from 30% in 2024, the reason being weak market sentiment and US tariff pressures. Still, 80% of IPOs delivered positive returns, raising Rs 67,737 crore so far.

CASE ANALYSIS

CASE 1: Urban Company IPO (2025)

- Issue Size: ₹3,000 crore

- Issue Price: ₹900

- Listing Price: ₹1,420 (57–60% premium)

Urban Company was listed on 17th September, 2025. If we take a look at Grey Market Premium (GMP) of ₹250–280 signaled that issue was underpriced. The issuers priced the IPO cautiously to ensure success amid overall weak market sentiment.

The company did a mix of fresh issue and offer for sale (OFS), with much of sale by existing shareholders. Sometimes existing shareholders price somewhat conservatively to ensure market acceptance.

Considering the profitability angle, Urban Company turned profitable in FY25 by registering a net profit of ₹240 crore, reversing losses in prior years. History has been witness that Investors are often more comfortable paying a premium when losses are being reversed and growth is visible.

To conclude Urban Company IPO is a strong example of underpricing, the issue price was modest relative to how aggressively the market bid it up.

CASE 2 Avenue Supermarts (D-Mart) IPO

- Issue Size: ₹1,870 crore

- Issue Price: ₹299/ share

- Listing Price (BSE): ₹604 (102% premium on listing day.)

The biggest case of IPO underpricing in India so far is widely considered to be Avenue Supermarts (D-Mart) IPO in March 2017. Avenue Supermarts’ underpricing wasn’t an accident. It was a deliberate, conservative strategy with a history of a very strong fundamentals.

Flashback to 2017 the retail consumption in India was booming in 2017 with rising middle-class income, urbanisation, and shift to organised retail this created perfect market timing.

The D-Mart IPO taught India that underpricing can be a powerful strategic move. By pricing conservatively, showcasing strong fundamentals, and leveraging promoter trust, a company can create both short-term and long-term wealth creation.

Conclusion

underpricing may be a rational trade-off to ensure a successful listing and investor goodwill, but excessive underpricing is costly. In my opinion firms should aim for transparent communication about business metrics.

In short, IPO underpricing in India is a multi-causal driven by market sentiment and strategic incentives. While it produces exciting listing-day headlines, the deeper question for markets and policymakers is how to balance initial market rewards with long-term price discovery and investor protection. The recent mix of spectacular debuts and high-profile disappointments suggests that while underpricing will remain a feature.